Ever wondered if you could receive more useful and meaningful reports from QuickBooks? Good financial information is not just a matter of convenience!

Nick is finding out that what he DOESN’T know about his financial system could pose a major setback to his business…

Nick’s “Unique” Profit & Loss Statement

“Wow, this is about the longest Profit & Loss Statement I’ve ever seen,” chuckled the loan officer as he flipped through another page on Nick’s company’s Profit & Loss report. Nick felt his face getting hot with embarrassment. Sitting in the banker’s office, hoping to secure financing for two major projects, was not the time he wanted to feel self-conscious!

“Wow, this is about the longest Profit & Loss Statement I’ve ever seen,” chuckled the loan officer as he flipped through another page on Nick’s company’s Profit & Loss report. Nick felt his face getting hot with embarrassment. Sitting in the banker’s office, hoping to secure financing for two major projects, was not the time he wanted to feel self-conscious!

Nick is counting on this loan to help expand his construction company. There are two really great projects that he can take on in the near future, but they are large ventures. He hopes to get a loan so that he can start both of them at about the same time. He’ll need financing if he hopes to make these two projects work.

“So, do you have job costing reports for your projects over the past 12 months? And can you tell me your average gross profit margin?” the loan officer asked.

The lender is implying that these are basic questions that he should know the answers to, so Nick has to think quickly about how to answer these inquiries. He doesn’t receive solid Job Costing reports from his accounting system, but he probably shouldn’t let the banker know that. He has a gut feeling that he’s probably making about 10% margins on his jobs but can’t be sure, let alone produce specific information for this meeting.

The lender is implying that these are basic questions that he should know the answers to, so Nick has to think quickly about how to answer these inquiries. He doesn’t receive solid Job Costing reports from his accounting system, but he probably shouldn’t let the banker know that. He has a gut feeling that he’s probably making about 10% margins on his jobs but can’t be sure, let alone produce specific information for this meeting.

So, he decides to assert calm and business-like confidence. Nick straightens his back, looks the banker in the eye, and replies, “Well, unfortunately, I don’t keep all of those details in my head, but I’ll have my bookkeeper pull that information together and send it over to you.”

What the Banker Needs From Nick…

“Good,” replied the lender, “I see you haven’t had a commercial construction loan before, so I’ll need to take your application to our loan committee. You’ll need to get these reports organized in a shorter and more standardized format – so that we can easily see your gross profit and net profit margins. We don’t want to have to wade through all of the details that you currently show on your company financials. I should also warn you that one of our ongoing compliance requirements is that we’ll need a full set of standard statements like that every quarter.”

“Good,” replied the lender, “I see you haven’t had a commercial construction loan before, so I’ll need to take your application to our loan committee. You’ll need to get these reports organized in a shorter and more standardized format – so that we can easily see your gross profit and net profit margins. We don’t want to have to wade through all of the details that you currently show on your company financials. I should also warn you that one of our ongoing compliance requirements is that we’ll need a full set of standard statements like that every quarter.”

“Where we WILL need the background cost details is when you apply for draws on the projects that we’re financing. As your project moves forward, we’ll be looking for reports that show estimated costs, change orders, and actual monthly and life-to-date costs for the various stages of the projects.”

Nick thanks the loan officer for his help, but as he leaves the bank, he feels a heavy weight on his shoulders. To move his business to the next level will be a huge undertaking. Sure, his in-depth construction experience, combined with his extensive community connections, has given his business a great foundation. It helps when it’s time to get contracts signed. But, to move ahead to grow his company, and to figure out how to meet these new financing requirements, leaves him with a nagging suspicion that he’s missing out on some “insider secrets” that he should know about.

Nick thanks the loan officer for his help, but as he leaves the bank, he feels a heavy weight on his shoulders. To move his business to the next level will be a huge undertaking. Sure, his in-depth construction experience, combined with his extensive community connections, has given his business a great foundation. It helps when it’s time to get contracts signed. But, to move ahead to grow his company, and to figure out how to meet these new financing requirements, leaves him with a nagging suspicion that he’s missing out on some “insider secrets” that he should know about.

He’s been thinking that his Job Costing reports aren’t the greatest, because he’s not making the year-end profit margin that he projected. Now, the banker is “raising his eyebrows” at the way his Profit & Loss is organized and presented.

He’s frustrated and annoyed that he wasn’t able to quickly and easily answer the banker’s questions. He’s worried that the reports he presented make him look like a novice, which is not the image he wanted to project when applying for a loan. And his lack of knowledge about his own business leaves him feeling vulnerable.

He’s frustrated and annoyed that he wasn’t able to quickly and easily answer the banker’s questions. He’s worried that the reports he presented make him look like a novice, which is not the image he wanted to project when applying for a loan. And his lack of knowledge about his own business leaves him feeling vulnerable.

What if he can’t get his information organized in the way the loan committee needs to see it? Will it mean that he can’t get the loan he needs to move ahead on his projects?

Consultant’s Corner

Like many business owners, Nick hasn’t been utilizing the full power of his QuickBooks accounting software program. He hasn’t set up a standard Chart of Accounts and a detailed background Item List. This is impacting his business reports in more ways than he can imagine.

How Did This Unfortunate Situation Occur?

..

Nick asked his bookkeeper – who hasn’t been trained in construction or job-cost accounting – to track his job costs. He told her all of the stages that a typical job goes through, and asked her to track costs that way.

Nick asked his bookkeeper – who hasn’t been trained in construction or job-cost accounting – to track his job costs. He told her all of the stages that a typical job goes through, and asked her to track costs that way.

So, given her limited level of knowledge, she’s done the best she could. She set up accounts that reflected those job stages in his Chart of Accounts.

While entering transactions, when she could see which costs went to which job and which job stage, she assigned the transaction that way. But, when she couldn’t figure it out, she simply assigned the costs to “Miscellaneous Job Costs”.

As a result, his Profit & Loss reports now show income and costs for activities such as “Site prep”, “Foundation”, “Framing”, “Cement work”, etc., plus “Miscellaneous Job Costs”. This has created a very extensive Chart of Accounts which results in a very long (and “non-standard”!) Profit & Loss report.

What Nick Didn’t Know About Standard Financial Statements and His Chart of Accounts

In the accounting and financial world, a standard profit and loss report would NOT show income and costs based on activities but, rather, would show costs in accounts such as “Direct Labor (Employment) Costs”, “Contracted Costs”, “Materials Costs”, “Other Direct Job Costs”, and “Indirect Production Costs”. You can imagine how this would result in a much shorter report. A simple change to show these types of accounts in his Chart of Accounts (rather than job-stages), would have yielded a standard Profit & Loss Report for Nick’s company. The report format would have been what the loan officer was used to seeing.

How QuickBooks Items Provide the Detailed Job-Cost Information that Nick Needs

BUT, you may be asking, if we remove all of that job-stage information from his Chart of Accounts, how would Nick track the job-cost activities and details that he DOES need to see – to monitor and run his jobs – and his business – more profitably? How does he track those costs if NOT through his Chart of Accounts?

That’s what the Item List feature is all about! What Nick didn’t know is that he (or his bookkeeper) could have established QuickBooks Items to track his job costs at a detailed level, while still recording costs in a more standardized format in his Chart of Accounts.

How Do QuickBooks Items Work?

Each Item in the Item List is linked to one or more accounts. For job-costing, these can be cost and/or income accounts. That means that if Nick (or his bookkeeper) records a job cost using an Item on the Item tab at the bottom of a Bill, Check, or Credit Card transaction, it is ALSO recorded in the linked account. Invoices also use Items, so income gets posted to the account linked to that Item.

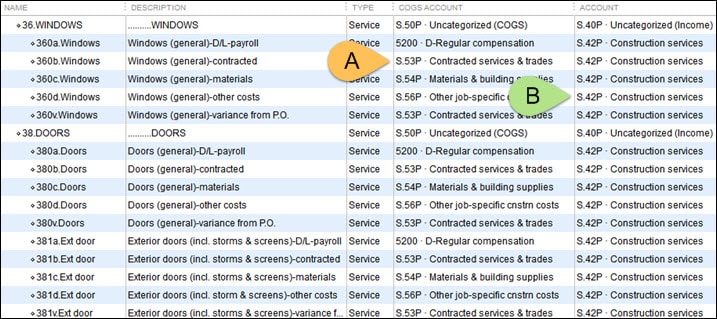

As Nick is the owner of a construction company, he can organize his Item List to see costs based on job stages and based on the type of cost within a job stage (example below shows Items linked to [A] cost and [B] income accounts).

Nick could also organize the list so that his jobs stages are sequential – that way his reports will reflect costs as they accumulate through the progression of his projects.

The result? By recording transactions using QuickBooks Items, Nick (or his bookkeeper) will be able to access and print reports in two different formats – one based on Items and one based on Accounts. Magic!

He can also use Items to identify Change Orders. AND, when it’s time to apply for loan draws, his Item-based reports will provide the detail that he needs for current and life-to-date information for each job stage.

What Else Has Nick Been Missing?

Nick doesn’t realize that he has other business information weaknesses that could be largely eradicated if he uses Items in combination with other QuickBooks features!

Using QuickBooks Items For Estimates

QuickBooks has an Estimating feature, and if you wish to use it, it requires that you use Items. If Nick establishes QuickBooks Items, instead of creating Estimates outside of QuickBooks, he could use Items to create Estimates within QuickBooks. That way he can see reports that will let him monitor “Estimate vs. Actual” Reports as a job progresses. He could use the information to help keep jobs aligned with his estimates and spot any Change Orders that haven’t been properly recorded. If he can’t bring a job back into line with the budget, at least he’ll know where his estimate differs from the actual costs so he can be more accurate on the next estimate.

QuickBooks has an Estimating feature, and if you wish to use it, it requires that you use Items. If Nick establishes QuickBooks Items, instead of creating Estimates outside of QuickBooks, he could use Items to create Estimates within QuickBooks. That way he can see reports that will let him monitor “Estimate vs. Actual” Reports as a job progresses. He could use the information to help keep jobs aligned with his estimates and spot any Change Orders that haven’t been properly recorded. If he can’t bring a job back into line with the budget, at least he’ll know where his estimate differs from the actual costs so he can be more accurate on the next estimate.

Using QuickBooks Items For Purchase Orders

Although the loan officer didn’t make it a condition for the loan, Purchase Orders can help Nick to define and control his costs for vendors, subcontractors, and other service providers. Purchase Orders (like Estimates) require the use of Items.

Fast Forward/Rewind

Based on the information we’ve provided you can likely now understand why Nick should have been using a standard Chart of Accounts combined with a well-designed QuickBooks Item List.

If he had, he would have walked into the banker’s office with much better information, and he would have been on top of his numbers. When the banker provided the “helpful” information about how he’d have to submit his quarterly reports and loan draw requests, he could have easily been able to say “No problem – we keep track of that on a day-to-day basis.”

If he had, he would have walked into the banker’s office with much better information, and he would have been on top of his numbers. When the banker provided the “helpful” information about how he’d have to submit his quarterly reports and loan draw requests, he could have easily been able to say “No problem – we keep track of that on a day-to-day basis.”

In this case, Nick bought himself a bit of time by saying that his bookkeeper would provide that information. But he’ll have quite a challenge to get everything fixed and shifted in his reporting system within the time frame he promised.

In this case, Nick bought himself a bit of time by saying that his bookkeeper would provide that information. But he’ll have quite a challenge to get everything fixed and shifted in his reporting system within the time frame he promised.

If, however, he’s able to rise to the challenge – now or in the near future – he’ll also become a more knowledgeable (and likely more profitable!) business owner. We’ll cheer him on, hoping that he’ll be able to make his changes in time to get his business loan…

Summary – How QuickBooks Items Create More Useful Financial Information

As we’ve learned from Nick’s dilemma, the QuickBooks Item list is critical for the smooth operation of three important business functions:

- QuickBooks Items allow information to be collected and presented in two very different ways:

- Profit & Loss Statements can be shown in a traditional format.

- Job-stage details can be shown in individual job-cost reports.

- Estimates: QuickBooks Items are used in (and required for) Estimates. When Estimates are entered into QuickBooks, you’ll be able to see Estimate vs. Actual variance reports. These reports give business owners ongoing control over job costs as well as longer-term help with future pricing decisions.

- Purchase Orders: QuickBooks Items are used in (and required for) Purchase Orders. As you likely already know, Purchase Orders are essential for defining and controlling costs.

Do YOU Have a Similar Problem?

Here are a few questions to ask yourself:

- Have you ever wished that you could produce a “real” (standard) Profit & Loss report every month – without help from your outside accountant?

- Are you frustrated because you can’t get useful, detailed job-cost reports? Or Estimate vs. Actual reports?

- How frequently does this happen?

- As a business owner or bookkeeper, how does this make you feel regarding your ability to confidently do your job and/or manage your business?

What if there was a fast and easy way that you could implement a bullet-proof Item List and Chart of Accounts for your construction business? Well, there is.

The solution: AccountingPRO.

The AccountingPRO system is specifically designed for construction business owners and bookkeepers who are too busy in their business to figure out how to organize the financial side of their business.

If you’re sick and tired of trying to run your business with a sub-standard set of numbers and missing financial data then now is the time to check out AccountingPRO.

Customer Praise For Diane Gilson, Info Plus Accounting, and BuildYourNumbers.com

⭐⭐⭐⭐⭐ From the Intuit FindAProAdvisor website:

“Diane’s knowledge of QuickBooks is amazing. I don’t profess to have an in-depth understanding of QuickBooks but when I talk with Diane, I quickly realize I don’t even scratch the surface. She has the ability & experience to quickly cut to the chase on fixing issues or setting up reports, estimates, items, lists, etc. Highly recommend her.”

See More Customer and Client Comments